A new breed of entrepreneurs is investing in social media stars, yielding volatile penny stock investments that are attracting teenagers. West of Hudson Group operates a network of content houses where many influencers live and has taken them public through a blank check company. This new trend seems to be begging for better scrutiny from regulators.

Read More

Chapter 15 allows foreign companies to file US bankruptcy proceedings to protect US assets. Over the past year, filings in Canada, Australia and the UK have spilled over to the US. While each country has its own unique set of laws, these cross-border links demonstrate the truly global nature of insolvency and the need to collaborate in this space.

Read More

The saga of student debt continues into the new administration. Here’s to hoping that it will be treated like any other debt in bankruptcy in the future, treating Education Department backed debts like any other unsecured debt, and affording fresh starts to all.

Read More

The concept of “Comparable Worth” as a way to equalize gender pay under Title VII has been discarded by US courts as too murky to implement. Meanwhile, in New Zealand, a woman-led government is finally making it law. It is about time that so-called “women’s work” is recognized and compensated for its skillful value-add.

Read More

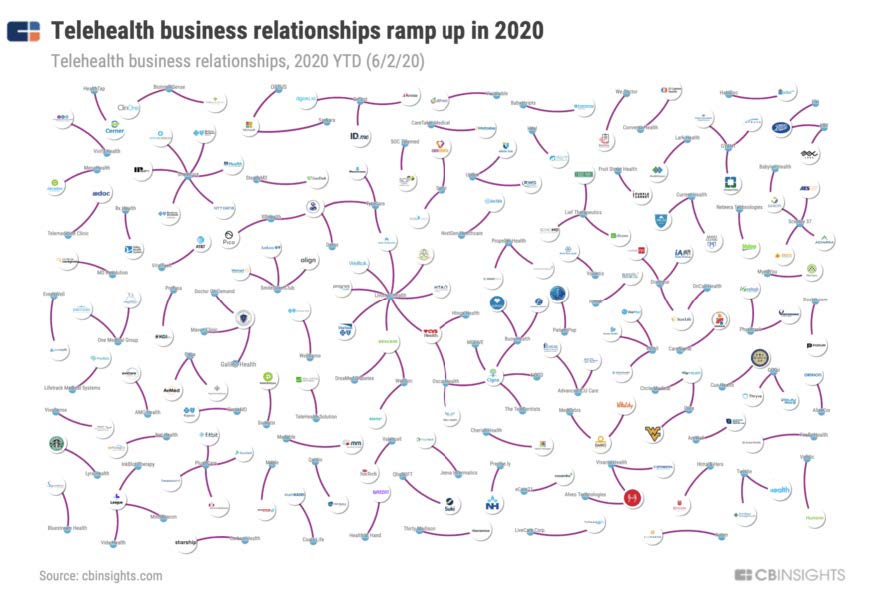

The “Digital Front Door” is a new integrated digital experience that empowers people to take an active role in managing their health. It is based on the use of personalized mobile and web platforms, many of them created by start-ups. Spurred by COVID-19, established healthcare systems have forged relationships with these start-ups, opening the door to enhanced care.

Read More

Thanks so much to the 15 start-ups that joined the Zoom Fireside Chat to discuss how to take their start-ups to the next level!

Read More

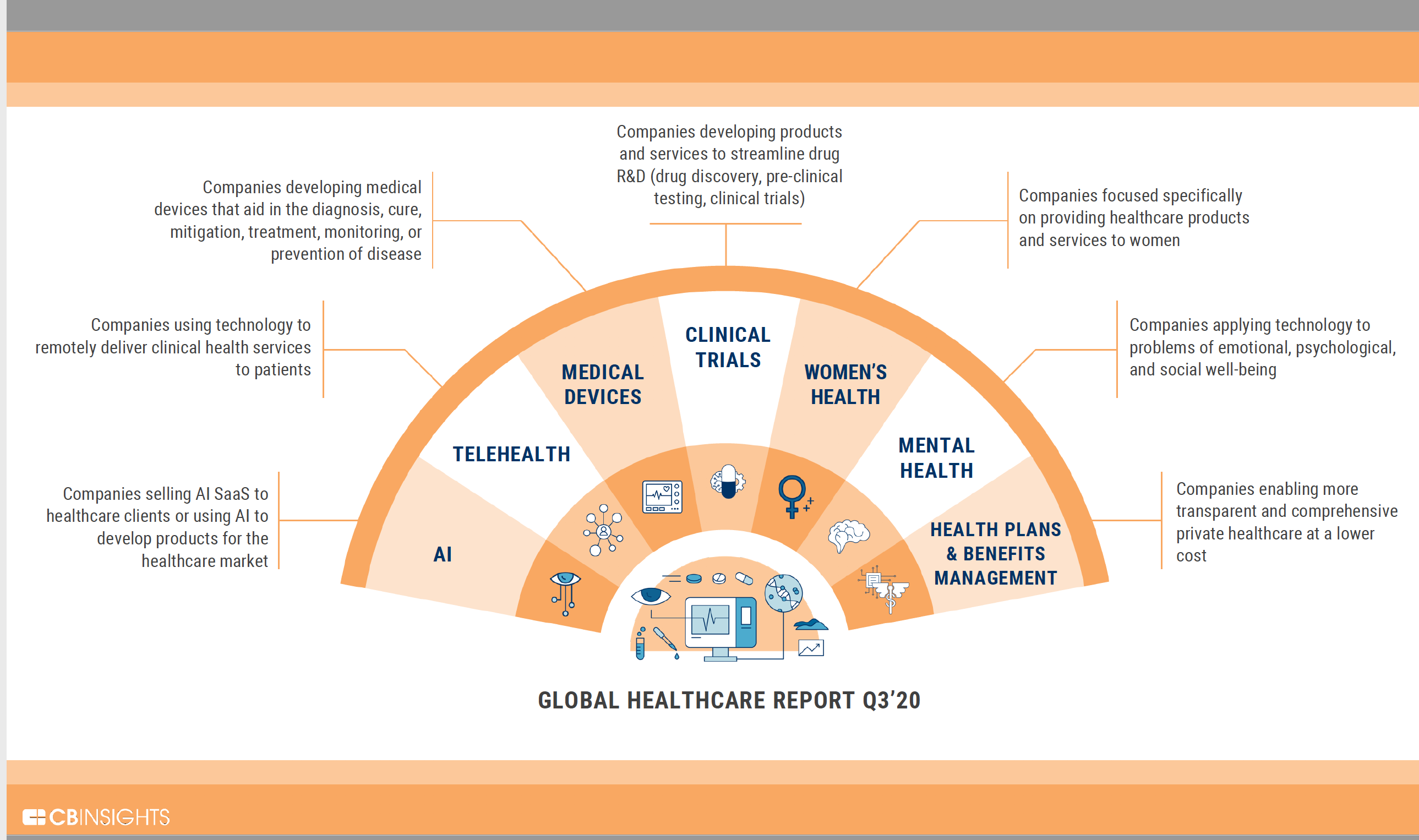

For those interested in a comprehensive yet concise survey of the various digital health sectors, unicorns, investors, trends and more, check out CB Insight’s State of Healthcare Q3’20 Report. Lots of infographics and charts, and lots of promising up and coming companies, including a focus on Women’s Health.

Read More

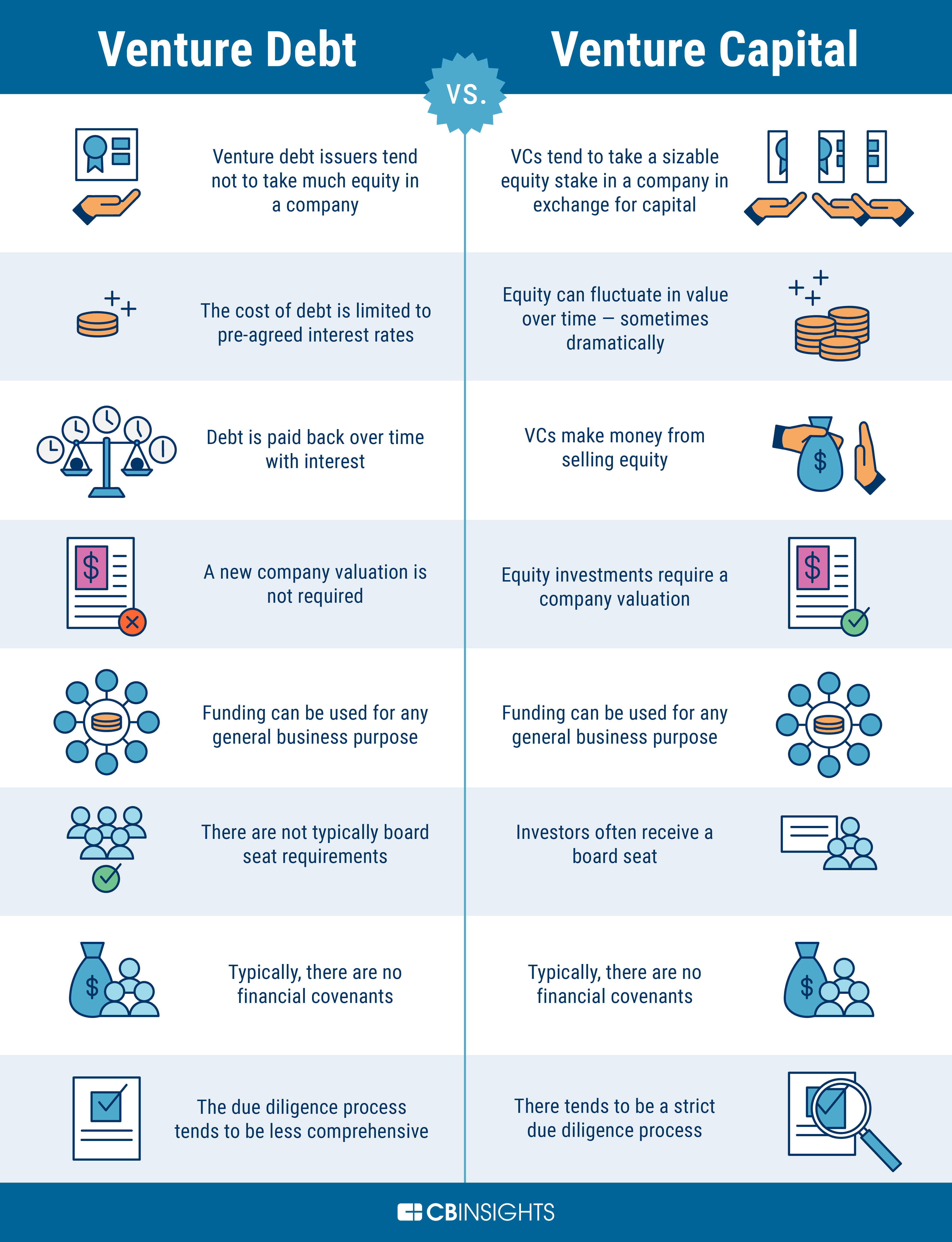

Venture Debt is a growing option for start-ups to access growth capital, while maintaining founder equity. The terms of Venture Debt include fixed repayment with interest secured by company assets, with a mild equity twist. This is a welcome trend, although piggy-backing on the prior infusion and support of Venture Capital.

Read More

Uber, Lyft and DoorDash have successfully obtained the CA vote to retain their workers as independent contractors, but they conceded to providing some “employee” benefits to obtain this milestone vote. This may be the beginning of a new model for independent contractor talent hiring in the growing gig ecosystem.

Read More

The SEC recently voted to expand its mission to help small business fundraise in private markets by increasing the threshold crowdfunding amount to $5M and the amounts that the non-accredited can invest. This new access is expected to boost entrepreneurship, now ever more present in our new normal of COVID-19.

Read More